Thought Leadership

APRWin is Not Infallible!

By: Joe Discenza

APRWin, from the Office of the Comptroller of the Currency, is a mainstay in compliance circles. It is a great tool, and, like nearly every field examiner in the Western Hemisphere, we use it nearly every day, right alongside our own Carleton APR validation tool. APRWin, however, is software, and all software makes trade-offs between being usable and being comprehensive; making best guesses as to the user's intent in unusual cases. In the unusual case where payments are due on the last day of one month, but not the last day of every month, APRWin guesses wrong.

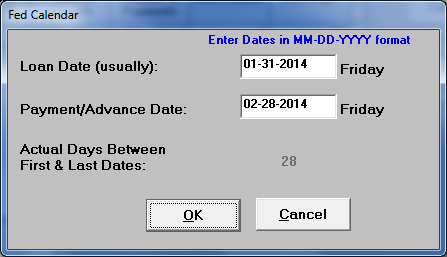

Consider a loan with $500.00 of Amount Financed as of July 31, 2014, with four payments of $150.00 each due monthly beginning August 28, 2014. Everyone would agree, and APRWin correctly determines, that there are twenty-eight days to the first payment. The APR (according to Appendix J's actuarial method, which is all APRWin knows how to do) is correctly computed as 95.2080% (to four places).

Wouldn't you think the APR would be exactly the same if you simply moved the entire loan, advance and four payments, six months earlier? APRWin doesn't!

Okay? Not so fast. APRWin, in the absence of further information, decides that this is one full calendar month (well, it is for the first interval), and that the subsequent payments are also full calendar months back to the contract date. With the rest of the payments scheduled on 3/28, 4/28, and 5/28, we know that isn't so, but APRWin doesn't.

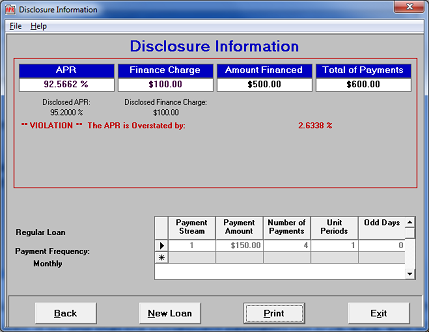

Now that's an overstatement that will get an examiner ex-“cited”! This can be somewhat ameliorated by entering the three remaining payments as a separate stream, but APRWin still miscalculates the time for the first payment and declares an “overstated” APR by 0.7428%.

The problem arises from exactly one shortfall: APRWin never asks for the scheduled payment date, and can only ask for the actual payment date. In Appendix J, section (b)(3)(iv) states, “If a series of payments (or advances) is scheduled for the last day of each month, months shall be measured from the last day of the given month to the last day of another month” (emphasis mine). With no way to ask for the scheduled payment date, it assumes that a payment on the last day of its month is scheduled for the last day of every month. Your dad taught you what 'assume' makes out of you and me, right?

A savvy examiner will recognize this, and hand-calculate the Unit Periods and Odd Days rather than relying on APRWin to do so. A savvy lender, presented with an overstatement notice (and, since APRWin always calculates a longer time period, it always understates the true APR), will ask the examiner to do so when a loan's payments are on the last day of some but not all months. You can move this same loan to 3/31 with payments scheduled on the 30th of the next four months and see the same behavior, just not as dramatically.

Joe Discenza is Senior Developer at Carleton and has an MS in Applied Mathematics (Optimization and Stochastic Processes) from the University of Michigan and two decades of experience in the lending calculation industry. He brings that expertise to both Carleton's Research Department and development of new software.