Compliance Alerts

April 2019

Effective State Changes

ARIZONA

HB 2177 was signed on April 1, 2019. It modifies the Arizona Regulatory Sandbox Program. Effective 90 days after adjournment.

HB 2418, approved on April 9, 2019, adds a provision to the Arizona Code requiring dealers to follow certain data protection requirements. Under the bill, dealers may submit or push data to manufacturers or third parties but may not allow these parties access to their dealer data system. The bill further restricts what a manufacturer or third party may do with the data they receive from a dealer. Effective 90 days after adjournment.

ARKANSAS

HB 1672 was approved by the Governor on April 8, 2019. The bill specifies that GAP waivers are not insurance. The bill includes definitions related to GAP waivers, requirements for offering GAP waivers, required disclosures, and cancellation requirements. Effective 90 days after adjournment.

SB 494 was approved on March 20, 2019 and establishes a $10 processing fee for the use of an expedited title processing service. Effective 90 days after adjournment.

IDAHO

HB 86 adds a sales tax exemption on a motor vehicle dealer's labor or service charges when installing accessories to new factory-delivered vehicles. Effective July 1, 2019.

IOWA

HF 260 was signed by the Governor on April 15, 2019. Under the Act, the threshold for the superintendent to establish the maximum rate of interest charges on consumer loans increases to an unpaid principal balance of $30,000 (up from $10,000). The act also includes a restriction on the collection of a minimum charge upon prepayment when the creditor has collected a service charge. Effective July 1, 2019.

INDIANA

The Department of State Revenue published Information Bulletin #28S regarding taxation of documentation fees in January 2019. Specifically, the bulletin states that “fees that meet the definition of a separately stated 'convenience fee' are not subject to sales tax.” But dealers may still charge a separate documentation fee, in addition to the convenience fee, which will be subject to sales tax. Effective April 2, 2019.?

MARYLAND

In 2018, Maryland established the Maryland Financial Consumer Protection Commission. Because the legislature failed to reauthorize the commission, it will sunset on June 30, 2019.

MICHIGAN

On December 18, 2018, Governor Snyder approved HB 6498. The bill is known as the “motor vehicle franchise act.” Under the act, among other provisions, a manufacturer is prohibited from preventing a dealer from charging a consumer a documentary preparation fee. Effective March 28, 2019.

MINNESOTA

The Minnesota Department of Commerce published guidance on licensing requirements in the state on April 5, 2019. The guidance formalizes the Department's requirement that a company that purchases retail installment contracts from Minnesota dealers must hold a sales finance company license. This applies to companies regardless of whether they have a physical presence in Minnesota. Effective for contracts executed after July 1, 2019.

NEW MEXICO

HB 6 was signed by the Governor on April 4, 2019. Among other tax-related provisions, the bill increases the rate of the motor vehicle excise tax. The applicable excise tax under the bill is 4% and is applied to the price paid for the vehicle or the reasonable value of the vehicle, under certain conditions. Allowances granted for vehicle trade-ins may be deducted from the price paid for the vehicle or the reasonable value. Effective July 1, 2019.

HB 150 became law on April 3, 2019. The bill applies to installment loans covered by the Installment Loan Act and the Small Loan Act. The bill expands annual lender reporting requirements and clarifies allowable loan insurance. The bill applies the limitation on permitted charges (not to exceed the lesser of $200 or 10% of the principal) specifically to a precomputed loan transaction, as opposed to simply “any such installment loan.” The bill prohibits any additional fee, interest or any other charge not specifically permitted for under the section. Effective July 1, 2019.

SB 350 was signed by the Governor on April 4, 2019. The bill amends definitions related to service contracts. It addresses a holder's right to return a service contract, refund requirements, and restrictions on automatic renewal notices. Effective 90 days after adjournment of the Legislature.

NEW YORK

SB 7074 was signed on December 28, 2018. The bill raises the threshold for the exclusion of the plain language contract requirement to agreements involving amounts of $100,000 or less. Effective for contracts entered into after June 26, 2019.

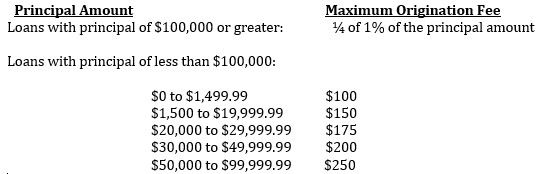

NORTH CAROLINA

SB 162 modifies the origination fee banks or savings institutions may charge for a loan or extension of credit not secured by real property to the following:

The bill states that a specific loan with a principal amount of less than $5,000, the APR shall not exceed 36%, inclusive of fees. The APR is to be computed in accordance with the Truth in Lending Act. There is no limit on fees for loans in excess of $300,000. The bill also amends late charges for loan contracts made by banks or savings institutions, limiting the amount of late charges for loans with an original principal balance of greater than or equal to $1,500, to: the greater of $35 or 4% of the amount of the payment past due. Effective immediately (April 1, 2019).

NORTH DAKOTA

HB 1195 creates contract requirements applicable to service contract providers. Effective on contracts entered after July 31, 2019.

HB 1292 amends the definition of “purchase price” as it relates to the application of sales or use tax. Effective July 1, 2019.

OKLAHOMA

The Department of Consumer Credit published dollar bracket adjustments. Included in the adjustments are the following:

Retail Installment Sales, § 2-201:

The greater of:

For loans subject to § 3-508(B) of the Oklahoma Code the maximum charge structure is:

Loan Amount Maximum Charge

The dollar amounts under § 3-508(A) remain the same.

The maximum delinquency charge for consumer credit sales and consumer loans will increase from $25.50 to $26.00. Effective July 1, 2019.

UTAH

HB 95 was signed by the Governor on March 25, 2019. The bill increases the collection costs for a dishonored check from $20 to $35. Effective 60 days following adjournment of the legislature.

VIRGINIA

SB 1325 was approved on March 25, 2019. The bill establishes requirements for offering GAP Waivers and includes provisions relating to disclosures, cancellation, and refunds. Effective July 1, 2019.

Update Reminders

OHIO

Ohio HB 123 applies to loans made after April 26, 2019. This affects Small Loans (§§ 1321.01-1321.19), Short-term Loans (§§ 1321.35-1321.48), and Second Mortgage Loans (§§ 1321.51-1321.60). The Act defines lending criteria for Small Loan Licensees, revises allowable fees, addresses restrictions for Short-Term Loan Licensees and adds disclosure requirements, among other requirements. Effective on loans made after April 26, 2019.

MASSACHUSETTS

HB 4086 went into effect on April 11, 2019. The bill established and modified certain laws regarding consumer financial and credit information.